The Efficiency of State Administration of Local Taxes

Key Findings

- Central administration of local taxes is a common feature of sales taxes but is less common for income, tourism, and other local taxes.

- Absent centralized administration, localities increase their administrative costs, impose substantial additional compliance costs on businesses, and reduce overall levels of compliance.

- A patchwork approach to local tax administration is particularly onerous for multijurisdictional businesses which often facilitate local transactions.

- Uniformity is increasingly important under Wayfair standards, especially as localities expand the use and definition of marketplace facilitators. Locally administered taxes create significant tax complexity, and in some cases, the expansion of these obligations on third-party platforms can raise constitutional concerns.

- Central administration benefits both taxpayers and governments, as it increases compliance, reduces compliance costs, and expands markets.

Table of Contents

Introduction

A mosaic of overlapping tax districts, differing tax rates, and multiple points of administration can make compliance with local taxes a daunting prospect—particularly for nonresident businesses.

The owner of a motel in Cartersville, Georgia, for instance, would have to collect a $5 per room lodging fee for each of her guests, remitting those collections to the state. Additionally, she would need to collect a local hotel and motel tax of 8 percent and remit it to the Cartersville city government.[1] She would also owe state and local sales tax on the transaction, remitted to the state. And, truth be told, she could probably handle this without too much difficulty, because she only operates in one jurisdiction.

But if she accepts a reservation through a booking website, the online agency that facilitated the transaction would be responsible for collecting and remitting these taxes. The agency would require a specific relationship with Cartersville, Georgia—and thousands of other jurisdictions across the country, each of which could potentially have different base, rate, compliance, and audit requirements.

By contrast, if this same motel were located in a place like Phoenix, Arizona,[2] all tourism taxes would be collected by the state government. Any booking website connecting people with hotel rooms, homestays, or any other activity subject to local tourism taxes could fully comply through state-level filings.

It is easy to see how local taxation can quickly become complex without one, central knowledge base, filing system, and set of rules, and many states have taken steps to simplify local administration on some level. An examination of the general landscape reveals that centralized collection administration of local sales taxes is common, reduces compliance and administration costs for localities and businesses, and does not adversely affect local revenue—in fact, it can even increase local revenue by giving cities and towns access to more of the market. Centralizing tourism and other local taxes is less common—which puts significant burdens on online platforms—but provides similar benefits to states.

Only Centralization of Local Sales Tax Administration Is Common

Thirty-one states are “home rule” states, and another nine have some home rule provisions. In these states, local governments have plenary grants of authority. They are free to enact whatever laws are not inconsistent with state or federal law, or where their authority has not been expressly proscribed. Generally, however, states remain free to adopt statutory restrictions on, or parameters for, local tax authority in these states.

It is only where there are constitutional enshrinements of home rule that give localities broad authority over their own organic law, as in Colorado,[3] where “home rule” and mandatory centralization of local tax administration can conflict. In a state like Colorado, it is hard for residents and even policymakers to appreciate just how unusual the state’s approach is, and how common it is for local taxes to be centrally administered. In fact, the benefits of central administration have made such a system prevalent among states for almost every kind of tax localities can levy—most commonly sales taxes, but many states centralize income and even lodging and tourism taxes.

It is important to recognize that home rule, in and of itself, is not a bar to centralized collection and administration of local taxes. And it is equally important to recognize that home rule is not a blank check for local tax administrators—even where constitutionally granted. Municipal tax authority in these jurisdictions is still constrained by federal and state constitutional protections of interstate commerce. Local jurisdictions may not adopt provisions that unduly burden remote transactions—like those facilitated by a booking website—even if they generally possess the authority to create their own tax systems.

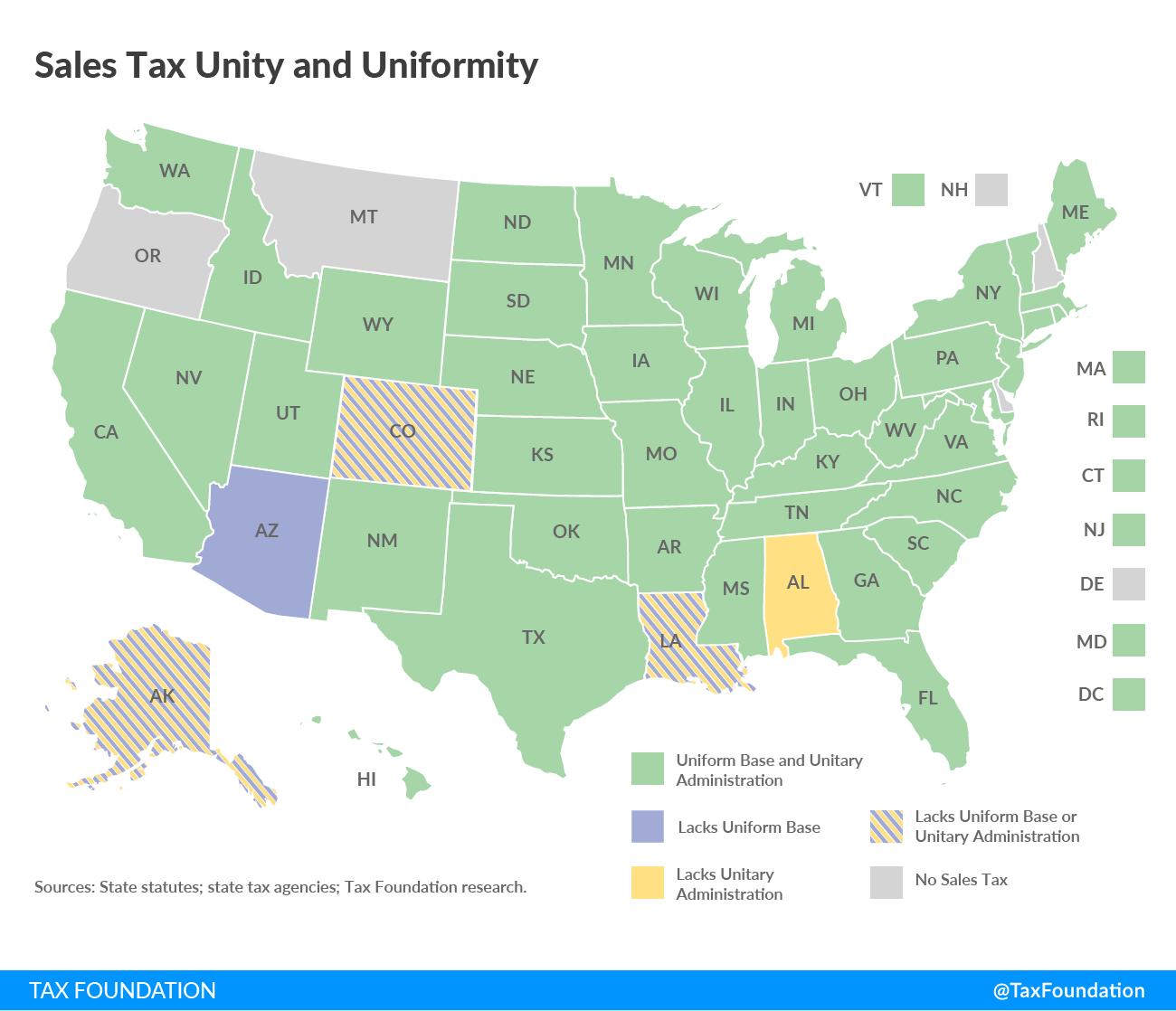

Of the 38 states that allow local option sales taxes (including Alaska, which allows sales taxes on the local, but not state, level), all but four states (Alabama, Alaska, Colorado, and Louisiana) collect sales taxes on behalf of localities. In Alaska, this is an outgrowth of the state’s decision to forgo its own sales tax but to grant the authority to localities. In the other three states, it stems from strong home rule traditions and constitutional grants of local taxing power. Central sales tax collection has historically been the norm for those states with centralized collection, but Arizona followed suit more recently when it consolidated its collection authority in 2017.[4]

{kind=link}

In some states, only select jurisdictions may impose a sales tax, while in others, a broad range of jurisdictions—counties, municipalities, and various local authorities—may opt, either by ordinance or local referendum, to impose one. Generally, these local sales taxes are levied on the same base used at the state level, and collections and administration are centralized within the state’s revenue agency, with the local share remitted to the municipality by the state collection authority. In many cases, moreover, states make it relatively easy to link a delivery address or geographic coordinates with a local rate through free software solutions that can be used on a standalone basis or through their integration with a variety of third-party vendors.

Although it is less prevalent for other tax types, centralized administration does not stop at sales taxes. Seventeen states allow local income taxes in addition to state-level personal income taxes. Most localities collect these taxes themselves, but six states collect income taxes on behalf of localities (see Table 1). These states allow residents to file their local and state taxes on the same form, simplifying the process for both taxpayers and the government.

Local tourism taxes, which tend to differ greatly between states, are also centrally collected in a number of states, as Table 1 shows. Thirty states levy their own lodging taxes, but a greater number of states give their local governments the authority to levy tourism taxes on meals, lodging, rooms, and other tourism-related transactions.[5] In these cases, the state sets parameters for what can be taxed, and localities can typically choose to levy the tax after presenting the question to voters.

| Local Sales Taxes | Local Tourism Taxes | Local Income Taxes | ||||

|---|---|---|---|---|---|---|

| State | Authorized | Centralized | Authorized | Centralized | Authorized | Centralized |

| Alabama | ✓ | ✓ | ✓ (a) | ✓ | ||

| Alaska | ✓ | ✓ | ||||

| Arizona | ✓ | ✓ | ✓ | ✓ | ||

| Arkansas | ✓ | ✓ | ✓ | |||

| California | ✓ | ✓ | ✓ | ✓ | ||

| Colorado | ✓ | ✓ | ✓ (a) | ✓ | ||

| Connecticut | ||||||

| Delaware | ✓ | ✓ (b) | ✓ | |||

| Florida | ✓ | ✓ | ✓ | ✓ (a) | ||

| Georgia | ✓ | ✓ | ✓ | |||

| Hawaii | ✓ | ✓ | ✓ | ✓ (a) | ||

| Idaho | ✓ | ✓ | ✓ | ✓ | ||

| Illinois | ✓ | ✓ | ✓ | ✓ (a) | ||

| Indiana | ✓ | ✓ (c) | ✓ | ✓ | ||

| Iowa | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Kansas | ✓ | ✓ | ✓ | ✓ | ✓ | |

| Kentucky | ✓ | ✓ | ||||

| Louisiana | ✓ | ✓ | (d) | |||

| Maine | ||||||

| Maryland | ✓ | ✓ | ✓ | |||

| Massachusetts | ✓ | ✓ | ||||

| Michigan | ✓ | ✓ | ||||

| Minnesota | ✓ | ✓ | ✓ | ✓ (a) | ||

| Mississippi | ✓ | ✓ | ✓ | ✓ | ||

| Missouri | ✓ | ✓ | ✓ | ✓ | ||

| Montana | ✓ | |||||

| Nebraska | ✓ | ✓ | ✓ | ✓ | ||

| Nevada | ✓ | ✓ | ✓ | |||

| New Hampshire | ||||||

| New Jersey | ✓ | ✓ (a) | ✓ | |||

| New Mexico | ✓ | ✓ | ✓ | |||

| New York | ✓ | ✓ | ✓ | ✓ | ✓ | |

| North Carolina | ✓ | ✓ | ✓ | |||

| North Dakota | ✓ | ✓ | ✓ | ✓ | ||

| Ohio | ✓ | ✓ | ✓ | ✓ | ✓ | |

| Oklahoma | ✓ | ✓ | ✓ | ✓ (a) | ||

| Oregon | ✓ | ✓ (a) | ✓ | ✓ | ||

| Pennsylvania | ✓ | ✓ | ✓ | ✓ (a) | ✓ | |

| Rhode Island | ||||||

| South Carolina | ✓ | ✓ | ✓ | |||

| South Dakota | ✓ | ✓ | ✓ | ✓ (e) | ||

| Tennessee | ✓ | ✓ | ✓ | ✓ (a) | ||

| Texas | ✓ | ✓ | ✓ | |||

| Utah | ✓ | ✓ | ✓ | ✓ | ||

| Vermont | ✓ | ✓ | ✓ | ✓ (a) | ||

| Virginia | ✓ | ✓ | ✓ | |||

| Washington | ✓ | ✓ | ✓ | ✓ | ||

| West Virginia | ✓ | ✓ | ✓ | ✓ | ||

| Wisconsin | ✓ | ✓ | ✓ | |||

| Wyoming | ✓ | ✓ | ✓ | ✓ | ||

|

(a) The state collects some, but not all, local tourism taxes. Sources: State statutes, forms, and instructions; National Conference of State Legislatures. |

||||||

Tourism transactions are often facilitated by a third-party provider, frequently on a central website that lets the user search dozens of airfare, hotel, or rental car companies simultaneously. Sometimes these third parties operate as facilitators and connectors for transactions that could also have been made separately, such as by booking directly with a hotel. In other cases, the platforms help create the market, with those letting rooms or providing the use of their car only accepting customers through these websites or apps.

In some cases, all details of a trip are organized by the central website, but the final payment is made by the customer when they arrive at the hotel—known as the agency model. In this way, the travel company avoids dealing with extra fees or changes made after the fact, like refunds for room changes or resort fees for activities. In other cases, especially for short-term rental platforms, the central website acts as the merchant, collecting payments and remitting necessary taxes. For these companies, keeping track of local taxes—many of which occur in overlapping jurisdictions—in all 50 states can quickly become overwhelming. Centralized administration relieves some of the burden.

Central administration, therefore, is a benefit to travel companies. But it is also good for local businesses and local governments too.

Central Administration Reduces Administrative and Compliance Costs

While the authority of tax collection might be attractive to many local governments, unified collection gives localities significant advantages. It reduces administrative costs, increases compliance, and potentially expands the market of tourism services, particularly in small jurisdictions.

Almost every tax collected at the local level is already also collected at the state level. Localities should take advantage of this preexisting infrastructure. Although states often use a portion of tax proceeds to pay to administer the tax, the efficiency of central administration means these costs are smaller than if the locality was funding its own administration. Paying to duplicate these systems, sometimes to capture revenue from a very small number of payors, siphons money and effort away from providing core services like police, fire, public schools, and local infrastructure. Everyone benefits when each level of government focuses on what it does best.

Centralized tax administration doubly benefits localities because more businesses will be able to comply with local taxes. Long gone are the days when the only people paying taxes to the county were the people living within its borders. With the rise of remote marketplaces, many sellers may conduct business with residents of a city without being intimately familiar with local taxes and regulations. This is especially relevant when taxing jurisdictions overlap, which could lead to confusion over expectations for even the most well-intentioned seller. A central repository of information and a single point of remittance better enable businesses to comply with local tax systems, providing localities with more revenue in the end.

Finally, for the smallest jurisdictions, an insistence on local administration can tip the scales on whether a local market exists at all. Multijurisdictional platforms must dedicate significant resources to research, engineering, registration, and other compliance tasks in even a small locality that administers its own taxes. Such a high cost of compliance may exceed an online marketplace’s revenue earned in a jurisdiction that may initially only support a few homeshares, for instance, if listing them would require the company to register with the jurisdiction and take on the compliance burdens associated with remitting local taxes. As a result, the marketplace may choose not to do business in this jurisdiction in the first place. Neither online marketplaces, which must limit their reach, nor local governments, which end up giving up tax revenue, are better off if tax complexity makes tourism services unprofitable.

Central Administration Does Not Expose Local Governments to Revenue Risks

A recent ballot measure to centralize local sales tax collection in Louisiana failed, with vocal opposition from local governments concerned about surrendering their authority over revenue collections.

Local groups often share the concern that instead of receiving every dollar they have collected, local governments that rely on state administration would have to put their collections in a common pool and rely on revenue sharing formulas to decide what portion of collections they would receive. Worse, they sometimes fear that the money may dry up entirely, with state governments “sweeping” the revenue into their own budgets during economic downturns, as a way to balance state budgets on the backs of the locals.

But they needn’t worry in this regard: there is a vast difference between statewide taxes with revenues that are distributed among localities and local-level taxes that are collected by the state. In the first case, the state is not just the tax administrator but the taxing authority, and local distributions are determined through the budget process, at the discretion of the legislature. In the second, the revenue never touches the state budget in the first place. Instead, the state simply acts as the tax administrator, disbursing revenue to the locality in which it was collected.

To illustrate this difference, we can look at the states of Connecticut and Arkansas. Connecticut does not allow local option sales taxes but does dedicate a portion of the state sales tax to share with localities.[6] The state’s Municipal Revenue Sharing Grant exists to distribute sales tax revenue with localities based on population and other factors. However, many local governments are unhappy with the system, as initial payouts were less than promised and further payout dates have been delayed several times.[7]

Arkansas, on the other hand, allows local option sales taxes and collects them on behalf of localities, as is the typical arrangement across the country. The revenue is tracked separately from state revenue,[8] with each locality receiving the amount of revenue that was collected within its jurisdiction.

Instead of taking revenue from municipalities, central administration brings in the same amount of collections while reducing administrative costs—a net positive for local governments. The costs per locality of a uniform state-run system are far lower than those incurred when each locality administers its own set of hospitality taxes. In fact, centralized collections may even generate more revenue if some transactions never took place because compliance costs were too high under a locally administered system.

Undue Local Tax Complexity Imperils Municipal Tax Schemes Post-Wayfair

Localities understandably want to benefit from the global marketplace of online sales, and 2017’s South Dakota v. Wayfair Supreme Court case did establish that states have the right to apply sales taxes to online commerce under certain conditions.[9] However, the issue of localities following suit presents some additional obstacles. Out-of-state retailers already face meaningful compliance burdens under each state’s sales tax requirements. And when obligated to juggle countless local tax administrations, the challenge becomes almost insuperable. In states with local sales tax administration, sellers may have to register for a license and remit taxes with each taxing unit, and even keep track of tax bases that differ between taxing districts. This imposes orders of magnitude more complexity than is found in states where sellers need to register only once with the state and remit tax collections to a central repository.

The Wayfair decision did not establish precise standards for the constitutional minimum requirements for states to require remote sellers to collect and remit sales taxes. However, the decision did highlight certain features of original South Dakota law that helped make the burden on remote sellers constitutionally light. States and localities have little to worry about in terms of legal challenges if they have a single point of collections and administration, a uniform base, and a simple, reliable way to identify the appropriate local tax rate. When states fall short of these standards of unity and uniformity, however, they impose considerable costs on remote sellers, reduce compliance, and likely run afoul of sellers’ constitutional protections.

Embracing uniform administration, on the other hand, benefits local governments in the end, as it reduces administrative costs and gives them access to a broader marketplace, including small sellers who would otherwise likely be out of compliance.

The statute at issue in Wayfair was about sales taxes, but the marketplace facilitator laws states have adopted since the decision have been expanded—and their logic extended—to require platforms or facilitators to collect a broader range of excise taxes. This can create serious challenges when the platform lacks the information necessary to remit certain excise taxes that are based on factors known only to the ultimate seller, or where the taxes are owed in the seller’s jurisdiction rather than the purchaser’s. It is particularly burdensome when these taxes are imposed at the local level, unlike most local option sales taxes. A local hotelier knows how to remit local tourism taxes; a third-party platform may find it difficult to identify all the obligations imposed on every single hotel owner in their network. If they are to remit these taxes, everyone, including the localities themselves, benefits from central administration, as it would make compliance—and even operations—possible for more sellers than a decentralized system could capture, leading to more—and more stable—revenue for localities in the long run.

Conclusion

Central administration of local taxes is common throughout the 50 states, and for good reason: such a system is an efficient way for localities to collect necessary funds, reducing both costs for local governments and complexity for businesses, while also increasing the share of the market that localities can access. The logic that has prevailed for local sales taxes should apply equally to other taxes that localities impose on multijurisdictional businesses, including local tourism taxes. The evidence is clear that central administration of local taxes reduces compliance costs without sacrificing local revenue.

References

[1] Georgia Department of Community Affairs, “Hotel-Motel Excise Tax Report,” May 2022, https://www.dca.ga.gov/sites/default/files/hotel-motel_tax_rates_and_revenues_5-17-22.pdf#page=2.

[2] Arizona Office of Tourism, “Transient Lodging Tax Rates: Arizona Communities,” January 2021, https://tourism.az.gov/wp-content/uploads/2021/01/Bed-Tax-Rates-Alpha-January-2021.pdf#page=2.

[4] Sales Tax Institute, “Centralized Licensing and Reporting of Arizona TPT Begins January 1, 2017,” January 2017, https://www.salestaxinstitute.com/resources/centralized-licensing-and-reporting-arizona-tpt-begins-january-1-2017.

[5] National Conference of State Legislatures, “Specific Statewide Taxes on Lodging – By State,” October 2020, https://www.ncsl.org/research/fiscal-policy/state-lodging-taxes.aspx.

[6] State of Connecticut, Office of Policy and Management, “Municipal Revenue Sharing Account,” https://portal.ct.gov/OPM/IGPP/Grants/Municipal-Revenue-Sharing-Account/Municipal-Revenue-Sharing-Account.

[7] Keith Phaneuf, “A pledge to share sales tax receipts with towns still goes unfulfilled,” Connecticut Mirror, Feb. 2021, https://ctmirror.org/2021/02/19/a-pledge-to-share-sales-tax-receipts-with-towns-still-goes-unfulfilled-was-it-a-case-of-fiscal-bait-and-switch/.

[8] Arkansas Department of Finance and Administration, “Sales and Use Tax Section, Distribution Report,” December 2022, https://www.dfa.arkansas.gov/images/uploads/exciseTaxOffice/LocalTaxDistribution_2022.pdf; Arkansas Department of Finance and Administration, “Sales and Use Tax Section, State Sales Tax Collections,” May 2022, https://www.dfa.arkansas.gov/images/uploads/exciseTaxOffice/Tax_Collections.pdf.

[9] Jared Walczak and Janelle Fritts, “State Sales Taxes in the Post-Wayfair Era,” Tax Foundation, December 2019, https://taxfoundation.org/state-remote-sales-tax-collection-wayfair/.

- The Benefits of Meal Prepping for Busy Moms - October 28, 2023

- The 11 Best Cash ETFs in Canada (Plus HISA ETFs and Money Market ETFs) - October 8, 2023

- Build a Variety of Outfits with These 7 Affordable Pieces - October 7, 2023